Faster Billing Software

For Your Fast-Moving FMCG Business

Make business operations Easy & Efficient with features designed for FMCG industry

myBillBook’s Most Useful Features for FMCG Stockists, Distributors, Wholesalers & Retailers

GST-Compliant Invoicing

Our software ensures that your invoices are fully compliant with GST regulations. Generate accurate invoices with GST identification numbers, product details, tax rates, and other required information.

POS Billing

Speed up your billing process at the point of sale with our user-friendly POS billing feature. Easily scan barcodes, process payments, and generate invoices in seconds. Improve customer service and enhance efficiency with our intuitive and fast POS system.

Inventory Management

Take full control of your inventory with our easy-to-use inventory management system. Monitor stock levels, manage a variety of products, and receive alerts for low stock. Optimise your stock management and avoid overstocking or stockouts.

Godown Management

Efficiently manage multiple godowns or warehouses with our dedicated godown management feature. Track stock movement between different locations, transfer stock and maintain accurate records of stock availability across your network.

Track Products With Batch Nos & Expiry Date

Our software allows you to assign batch numbers, set expiry dates, and generate reports to help you manage inventory rotation effectively. Also, minimise losses due to expired products.

Generate Purchase Invoice

Simplify your purchase process with our purchase invoice feature. Generate purchase invoices, track vendor payments, and maintain a clear record of your procurement activities. Streamline your purchase workflow and improve vendor management.

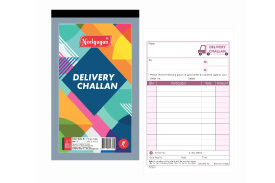

Delivery Challan

Manage your product deliveries seamlessly with our delivery challan feature. Create delivery challans, track shipments, and ensure accurate order fulfilment. Enhance customer satisfaction and maintain transparency in your delivery process.

Barcode Generation & Printing

Effortlessly generate and print barcodes for your products using our software. Streamline your inventory management and sales processes by scanning barcodes for quick and accurate product identification, pricing, and tracking.

Record Payment In & Out

Keep track of all your financial transactions with our payment management feature. Record both incoming and outgoing payments, including cash, card, and online transactions. Easily reconcile payments, maintain accurate records, and track outstanding payments.

Get Clear Business Insights

Gain valuable insights into your business performance with our comprehensive reporting module. Generate detailed reports on sales, purchases, inventory, profits, and more. Analyse trends, identify opportunities and make data-driven decisions to drive business growth.

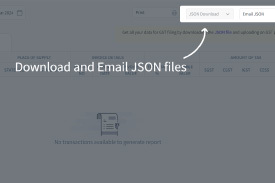

GSTR-1 in JSON Format

Our software provides seamless integration with the GST portal. Generate GSTR-1 reports in JSON format directly from the software, ensuring easy and accurate GST return filing. Stay compliant with GST regulations without the hassle of manual data entry.

Staff Attendance & Payroll Management

Efficiently manage employee attendance and automate payroll calculations with our integrated attendance and payroll management feature. Track attendance, record leaves, and generate payroll reports, ensuring timely and accurate salary calculations for your employees.

Hear Directly From Our Users From FMCG Industry

FAQs on FMCG Billing Software

What is FMCG billing software?

FMCG billing software is a specialised software solution designed to streamline billing processes for Fast-Moving Consumer Goods (FMCG) businesses. It automates invoicing, inventory management, POS billing, and other essential functions specific to the FMCG industry.

What are the benefits of using FMCG billing software?

FMCG billing software offers several benefits for businesses, including:

- Faster and more accurate billing processes

- Improved inventory management and stock tracking

- Compliance with GST regulations and seamless tax filing

- Enhanced customer experience through efficient POS billing

- Real-time reporting and analytics for informed decision-making

Is FMCG billing software customisable?

Yes, our FMCG billing software offers customisation options to meet the specific requirements of different businesses. You can personalise the software to match your workflows, branding, and unique business needs.

Can FMCG billing software handle multiple locations or branches?

Yes, our FMCG billing software is designed to accommodate businesses with multiple locations or branches. It allows you to manage and track inventory, sales, and billing across different sites from a centralised system. This feature ensures consistency in pricing, stock management, and reporting, providing a holistic view of your business operations.

Is training and support available for FMCG billing software?

Yes, we offer training and support services to assist businesses in implementing and utilising the software effectively. We provide onsite demos, onboarding training, and documentation to help you understand the software’s features and functionalities. Additionally, customer support teams are available to address any queries, issues, or technical assistance you may require during the usage of the software.